The worst part about credit default swaps is their inaccessibility to unsophisticated investors. At least, I think that’s what ProShares had in mind when they launched their credit default swap ETFs yesterday.

TYTE buys swaps on the CDX index. WYDE sells CDX swaps. I’m not making this up.

CDX is an index that tracks North American credit default swaps. Traders who buy or sell TYTE and WYDE don’t actually own or act as counterparty to credit default swaps, of course. CDX is based on a synthetic bond with fixed coupon payments. It is made up of 100 CDS issuers, and if there’s a credit event, the sellers pay off the buyers, and the index is restructured with new CDS and a new base price.

Who needs hedge funds when individual investors can make Big Shorts from the comfort of our 401k accounts?

Last month, Kleiner Perkins finally added Uber to their portfolio. Uber joined their Digital Growth Fund alongside other winners like Facebook, Groupon, Twitter, and Zynga [1]. And before you point out that 50% of those companies are shit, remember that the important part is that KPCB got out at IPO. (oh, I guess they held on to some common stock)

KPCB participated in Uber’s $1.2B Series D round at a valuation of $17B. The fund also did not invest in Facebook or Twitter until fairly late in the game. Does this A-list portfolio make Kleiner Perkins a good VC firm? Is Mary Meeker, who leads the Digital Growth Fund, a good VC?

VCs expect their investment returns to take a power law distribution, where a stake in just one company achieves a valuation greater than the entire fund [2]. Not only do VCs usually exercise their pro rata rights in up rounds, but startups that have up rounds tend to attract bigger and better investors, accumulating advantage and cementing future success.

VC firms also take a power law distribution. A firm that makes a good early investment (eg, Kleiner Perkins with Google) will have an easier time raising future funds and gain access to better deals. A company like Uber has its choice of investors. It wasn’t trying to fill board seats, but a bank account, and went for the biggest VC names in the industry.

3 percent of the venture capital firms generate 95 percent of the industry’s returns, and the composition of the top 3 percent doesn’t change much over time [3].

Good VCs don’t have to pick good companies to invest in; Good companies choose them as investors.

In 1985, Intel was a semiconductor memory company. It had been a memory company for 17 years, but Japan was making memory better and cheaper and Intel was bleeding money trying to keep up. After over a year of experimenting with futile strategies, president Andy Grove and CEO Gordon Moore fired themselves.

They walked outside, smoked a couple cigarettes, and then walked back in pretending to be new hires. The pretend-new CEO and president didn’t know that Intel spent 17 years selling computer memory. They took one look at the company, killed the memory business, and used their freshly-freed talent to become a microprocessor company.

You’re fired. For the porn ‘stache.

Anchoring is a cognitive bias that forces people to focus on some initial value and then make decisions with that reference. A good salesman often quotes an inflated price and then allows the customer to negotiate a much lower price. Because the customer has the initially-quoted price as an anchor, the new price seems like a great deal.

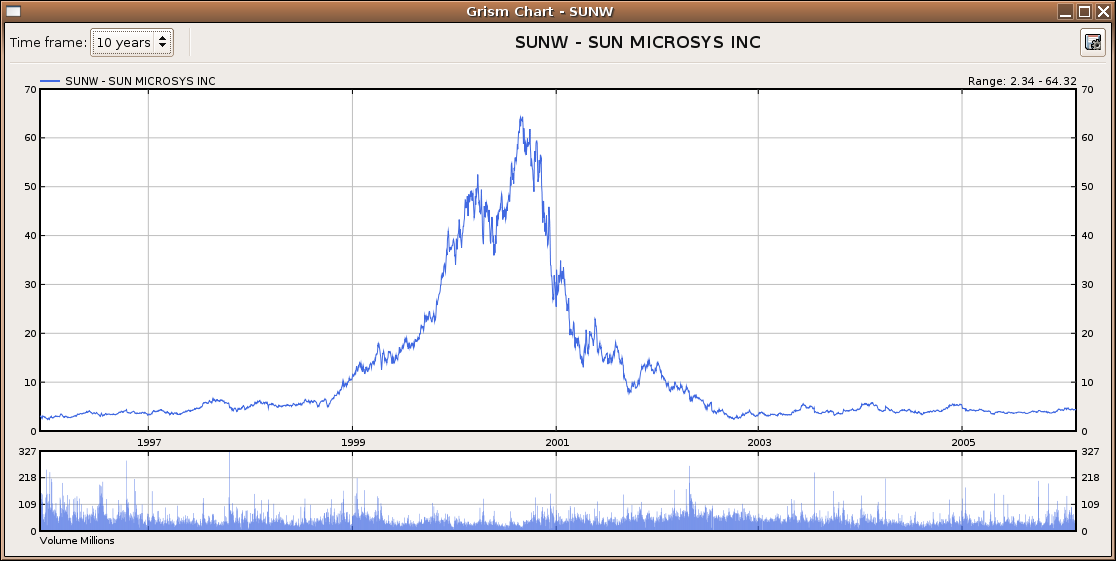

As a novice investor, I didn’t want to realize my loss. If I didn’t sell Sun, it was hypothetically still worth my anchoring purchase price (even though the market was trading at half that). My very smart labmate Andy asked me: If you didn’t already own this stock, would you buy it today?

Of course not. It was a shitty company and nobody liked Java.

So sell it.

Avoid anchoring biases by framing the situation in a new perspective. If your employer fired you, is this the job you would look for today? If not, quit. If your spouse died, is this the replacement you would look for on OKCupid? If not, leave. If your child died, would you make another one? If not, put it up for adoption.

If you were starting a new company, is this the one you would start today?

Nobody thinks about Silicon Valley as much as Silicon Valley. Venture capital is less than 3% the market cap of the NASDAQ and less than 1% of total US equity. Who cares if VCs aren’t funding cancer research?

Real innovation gets its funding elsewhere. The financial industry has been one of the largest benefactors of data science. The porn industry was a huge driver of internet technology.

My research grant at the University of Sydney came from a hedge fund. Something to do with machine learning and algorithmic trading. We don’t much like high-frequency traders, but it’s hard to argue the merits of machine learning research.

Back before VC firms even existed, tobacco companies generously funded medical research on heart disease and stress. Back then, doctors recommended smoking as a cure for stress.

When it comes down to it, I just want to build cool stuff. I’m a Nerd.

Peter Thiel characterizes two dichotomous personality types: Nerds and Athletes. Nerds are motivated by the act of creation, Athletes by competition. Competition is inherently destructive because a competitor only wins if someone else loses.

The definitions have nothing to do with technical or physical ability, but personal tendency. Nerds avoid fighting (probably because they got their asses pummeled a lot as kids), and athletes seek out competition because they have a history of being good at it.

A fighter says, Let’s disrupt the mousetrap industry by building a better mousetrap. A nerd says, Let’s build a cat. Well, not a cat, because cats are lame, but maybe a mouser, or a flying spaghetti monster.

Athletes

Truly disruptive technology is created by nerds. Because nerds go out of their way to avoid fighting, they build things where competition hasn’t begun to look.

But organizations need both nerds and athletes. A company full of fighters would self-implode. In a world with only creators, socialism might be a fine institution. But when the competitive athletes come along, companies full of nerds get steamrolled.